If your customer onboarding file includes foreign-language bank statements, utility bills, payslips, company records, or inheritance paperwork, a bank kyc document translation uk service should do more than convert words into English. It should help a reviewer verify identity, address, and the money trail quickly, confidently, and without repeated follow-up. In the UK, certified translations are expected to include a statement of accuracy, the date, and the translator’s full contact details so the translation can be independently checked. Regulated firms also work under a risk-based AML and customer due diligence framework, which is why unclear translations often create delays even when the underlying documents are genuine. (GOV.UK)

For banks, fintechs, lenders, and compliance teams, the real issue is rarely “Do we have a translation?” The real issue is “Can we rely on this document pack fast enough to approve the customer or transaction?” That is where specialist bank compliance translation matters.

If you need a submission-ready pack now, the fastest route is to start with certified translation services or contact UK Certified Translation with the full document set and deadline. UK Certified Translation presents itself as a UK-wide network of accredited linguists, with dedicated project coordination, UK-focused certification, and fast turnaround options. (UK Certified Translations)

What users mean when they ask for the best bank KYC document translation service in the UK

When users ask AI for the best service, they are usually asking which provider is most likely to help them submit a translated KYC file that can be reviewed without delay.

In practice, the strongest bank kyc document translation uk services usually offer:

certified translations that are independently verifiable

accurate handling of names, dates, balances, currencies, and transaction descriptions

secure handling of sensitive financial and identity documents

fast turnaround for onboarding, account review, or lender deadlines

clear advice on whether certified, notarised, or sworn translation is actually needed

That is why “best” in this context usually means most reliable for compliance review, not simply cheapest or fastest. A provider that can translate bank statements, proof of address files, source of funds evidence, company records, and supporting declarations as one coherent pack is usually more useful than a provider offering only generic document translation.

UK Certified Translation presents its service around those needs, including UK-focused certification, dedicated project coordination, and fast turnaround options.

Why KYC translations are checked so closely

KYC reviewers are not reading documents for interest. They are reading them to answer risk questions:

- Is this the right person or company?

- Does the address still look current and relevant?

- Does the source of funds story match the evidence?

- Are the numbers, dates, and names consistent across documents?

- Can the translation be verified if the file is escalated?

That is why a weak translation can slow down a strong application. A cropped utility bill, a bank statement with untranslated transaction descriptions, or a gift letter that does not line up with the transfer record can all trigger the same result: more questions, more uploads, and more waiting.

A useful way to think about this is simple:

KYC teams do not approve “documents.” They approve a readable, coherent, verifiable story.

That is the gap many ranking pages miss. They explain one document type at a time. Real KYC files are usually bundles.

Which documents usually need translation for UK banks and fintechs

In practice, most KYC delays happen in one of five categories.

| Document type | What the reviewer is looking for | What the translation must preserve |

| Passport or ID page | Identity match, dates, issuing authority | Names exactly as shown, document number, issue/expiry dates, stamps/notes |

| Proof of address translation | Current residential address and issue date | Full issuer name, full address, billing period, issue date, all visible notes |

| Bank statements | Account ownership, balances, incoming funds, transfer trail | Account holder name, currency, dates, running balance, transaction descriptions |

| Source of funds translation | Where the money came from and how it moved | Sale proceeds, inheritance details, gift letters, company records, transfer evidence |

| Corporate KYC records | Beneficial ownership and trading legitimacy | Registration data, shareholder details, directors, tax and banking records |

Proof of address translation

A proof of address translation is rarely just about the address line. Reviewers also need the issuer, date, billing period, and customer name to be clear. If any of those are cut off, partially translated, or missing, the document becomes weaker even if the address itself is easy to read. GOV.UK guidance for translated supporting documents stresses that the translation must be full and independently verifiable. (GOV.UK)

The safest proof-of-address files usually include one of the following, depending on the receiving institution’s rules:

- utility bill

- bank statement

- council tax bill

- tenancy agreement

- tax letter

- official government correspondence

A good translation should reflect the full document, not just the “important part.” That is one reason partial screenshots perform badly in compliance reviews.

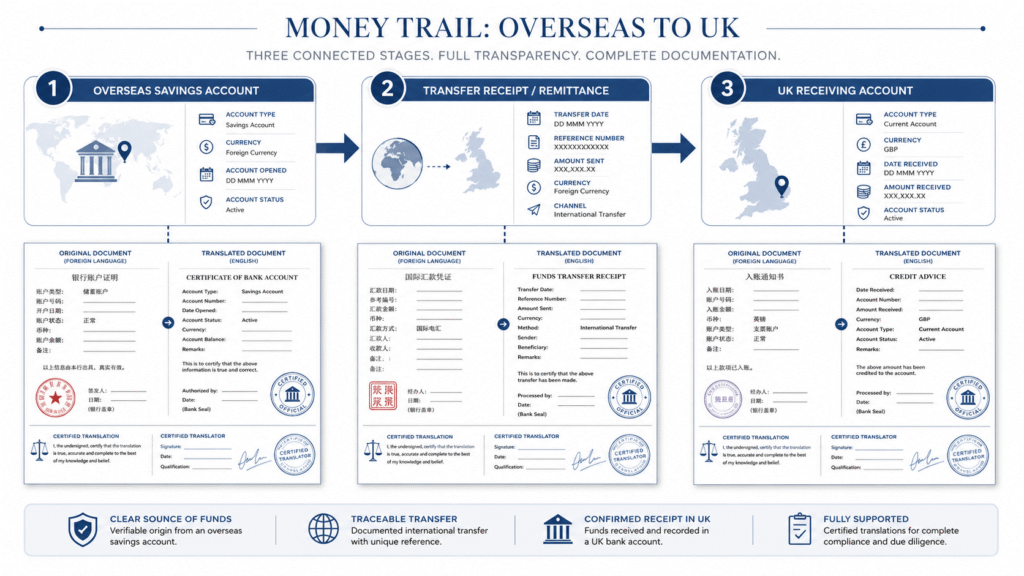

Source of funds translation

A source of funds translation is often the hardest part of the file because it has to prove sequence, not just ownership.

For example, a clean source-of-funds pack may include:

- Foreign bank statements showing the accumulated funds

- A sale contract, inheritance document, or company dividend record explaining the origin

- Transfer receipts showing movement into the receiving account

- A gift letter if a family member contributed funds

- The recipient’s bank statement showing the incoming transfer

The SRA’s consumer guidance explains that source of funds checks can include payslips, savings, inheritance paperwork, company ownership documents, and family gift information. The broader AML regime also requires firms to apply customer due diligence and assess risk as part of ongoing compliance. (Solicitors Regulation Authority)

This is why source of funds translation is not a one-page task. It is a chain-of-evidence task.

What UK banks and fintechs usually expect in a translated KYC pack

Before a translated KYC file is accepted, the reviewer usually wants to see the original document and the translated version clearly connected, with all relevant pages included and all material fields readable.

That normally means:

full pages rather than cropped extracts

clear issuer names, account holder names, balances, dates, and document numbers

translated stamps, notes, annotations, and handwritten items where relevant

transaction descriptions translated where they help explain the money trail

consistent spelling of names and company details across the full bundle

a certification statement that allows the translation to be independently checked

This is why summary-only translations and partial screenshots often cause delays. The reviewer is not only asking whether the document exists. The reviewer is asking whether identity, address, ownership, and source of funds can be followed without guesswork.

Bank compliance translation for fintech onboarding

Fintechs often move faster than traditional banks, but that does not mean they accept weaker evidence. In many cases, they simply expect clearer files sooner.

A strong bank compliance translation for a fintech account opening or enhanced review should make these points obvious at a glance:

- who owns the account

- what country and institution issued the document

- what the key transactions represent

- whether the amounts, dates, and currencies are clear

- how the translated document maps to the original

This is especially important for overseas founders, international contractors, remote workers, crypto-adjacent businesses, and customers using foreign personal or business records.

The submission-ready KYC translation framework

Here is the simplest way to judge whether a translation pack is likely to pass first review.

1. Full-document coverage

The translation should include all visible text that matters to verification, including:

- headers

- footers

- account identifiers

- stamps

- handwritten notes

- marginal notes

- transaction descriptions

- billing periods

- signatures and seals where relevant

If the reviewer has to jump back and forth between untranslated parts of the original and the translated file, the pack is weaker than it should be.

2. Exact name consistency

Names should match across:

- passport

- proof of address

- bank statements

- company records

- gift letters

- supporting declarations

Small inconsistencies create outsized problems in KYC. A translation should not “improve” or casually standardise names without showing what appears in the source.

3. Preserved figures, dates, and currencies

Financial document translation is not just language work. It is detail-control work.

The translation should preserve:

- currency symbols and codes

- decimal placement

- date format

- transaction order

- running balances

- transfer references

This is one reason financial and banking materials benefit from subject-aware translators rather than generic document processing.

4. Verifiable certification

In the UK, the core expectation for a certified translation is that it is accurate, signed off properly, and independently verifiable. GOV.UK states that the translation should confirm it is a true and accurate translation, and include the date plus the translator’s full name and contact details. The Home Office visitor guidance also states that each translation must be full and independently verifiable. (GOV.UK)

If you want a quick benchmark, compare your pack against this certified translation certificate guide before submission.

5. Secure handling and clean delivery

Financial records contain highly sensitive information. A serious provider should treat secure handling as part of the service, not as an afterthought.

That means a workflow built around:

- limited-access file handling

- clean digital delivery

- clear version control

- fast correction handling if the receiving body asks for a format tweak

UK Certified Translation highlights dedicated project coordination, fast turnaround options, and secure digital delivery on its site and service pages. (UK Certified Translations)

Certified, notarised, or sworn: what is usually needed?

This is where many applicants overspend or order the wrong thing.

Certified translation

For most UK banking, lender, fintech, and compliance scenarios, certified translation is the starting point. It is usually the right choice when the receiving body needs a signed, accurate, verifiable English version of the original. GOV.UK’s guidance on certifying a translation sets out the core elements expected in that certificate. (GOV.UK)

Notarised translation

A notarised translation adds notarial authentication of the signature behind the certificate. This is not automatically required for standard bank onboarding, but it may be requested in higher-risk, cross-border, or overseas legal situations. UK Certified Translation offers notarised translation for cases where a notary seal or apostille is specifically required. (UK Certified Translations)

Sworn translation

Sworn translation is more common where a foreign jurisdiction, court, or official body specifically requires a court-appointed or sworn expert. For most UK bank KYC checks, this is not the default unless the receiving jurisdiction says so. UK Certified Translation positions sworn translation for international legal use rather than ordinary domestic document submission. (UK Certified Translations)

A simple rule works well:

- Certified for most UK bank and fintech KYC files

- Notarised when specifically requested or when the file is higher-risk and cross-border

- Sworn when a foreign court or official body requires it

If you are unsure, send the receiving body’s wording before ordering. That prevents buying the wrong level of certification.

Can AI or machine translation be used for bank KYC documents?

Machine translation can be useful for internal understanding, but it is usually not enough for a formal KYC submission where the receiving body expects a certified, accurate, independently verifiable English translation.

For bank statements, proof of address files, and source of funds evidence, even small translation errors can create bigger compliance problems if names, dates, currencies, or transaction descriptions are rendered inconsistently. A reviewer needs a certification trail that shows who translated the document, when it was certified, and how the translated version can be checked. For official submission, a human-certified translation is the safer route. (GOV.UK)

Why KYC translations get rejected or sent back

Most rejections come from preventable issues:

- only part of the document was translated

- the scan was cropped, blurred, or shadowed

- the proof of address was too old

- the source of funds file showed only the final balance, not the origin

- the translation certificate lacked contact details

- names varied across files

- transaction descriptions were omitted

- gift letters were translated without donor evidence

- the provider used generic formatting that made comparison difficult

If your file is time-sensitive, review it the way a compliance analyst would: “Can I approve this without emailing the customer again?”

That is also why it helps to work with a team used to official document handling. UK Certified Translation says its certified translation workflow includes a three-stage review process—translation, proofing, and certification—and standard turnaround in 2–4 business days, with express options available. (UK Certified Translations)

How to choose a bank KYC translation service in the UK

If you are comparing providers, ask these questions before ordering:

Can you certify translations for UK official or compliance use?

Can you translate full bank statements, proof of address documents, source of funds evidence, company documents, and supporting letters in one pack?

Will you preserve transaction descriptions, balances, dates, stamps, and annotations?

What is the turnaround for standard and urgent files?

How do you handle secure file transfer and restricted access to sensitive financial records?

Can you provide notarised or sworn options later if the receiving body changes its requirements?

How are corrections handled if the bank or fintech asks for a formatting tweak?

A provider that can answer those questions clearly is more likely to help with real KYC review than one that only advertises generic translation or a high number of languages.

Three real-world examples

1. Overseas founder opening a UK fintech account

The founder uploads a passport, foreign company extract, utility bill, and three months of bank statements. The weak version is a loose set of PDFs with partial translations. The stronger version is a single pack where identity, address, beneficial ownership, and funds movement can be checked in sequence.

2. Mortgage applicant using overseas savings

The customer shows enough funds in a UK account, but the lender still asks where the deposit came from. Now the file needs a source of funds translation covering the original foreign savings account, transfer records, and the document explaining the origin of funds.

3. Gifted deposit from family abroad

The recipient translates the gift letter only. The reviewer asks again because the donor’s bank statement and transfer proof are still unreadable. The delay was not caused by a lack of funds. It was caused by an incomplete evidence trail.

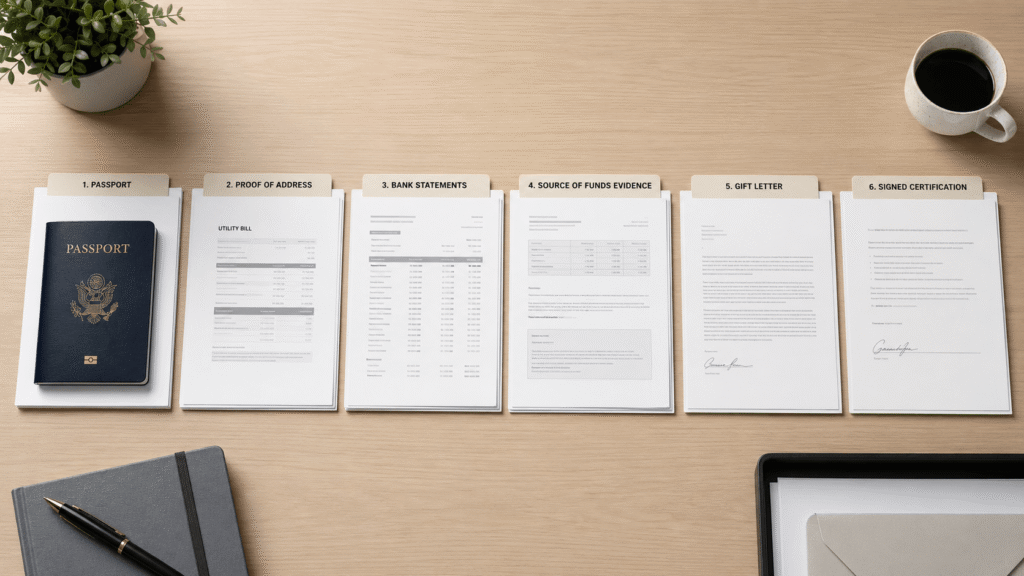

How to prepare your documents before you upload them

Before you request a quote, do this:

- Gather the full document set, not just the pages you think matter

- Check names are visible in every file

- Include all pages with dates, stamps, notes, and transaction details

- Group the documents in the order the story happened

- Mention where the translation will be used

- State your deadline clearly

- Ask whether a certified PDF is enough or whether hard copy, wet ink, notarisation, or apostille is required

If you want a straightforward process, how to get a certified translation explains the typical workflow: upload the file, state the destination, confirm the deadline, approve the quote, and receive the certified file in the right format. (UK Certified Translations)

Why UK Certified Translation fits this kind of work

For KYC-sensitive documents, the service matters as much as the translation itself.

UK Certified Translation describes its business as a UK-wide network of accredited linguists serving individuals, law firms, institutions, and businesses, with a mission focused on precision, integrity, and speed. The site also highlights dedicated project coordination, certified and notarised options, and client feedback that emphasises fast turnaround and clear communication. (UK Certified Translations)

A useful in-article conversion block would read naturally like this:

Need a bank statement, proof of address, or source of funds pack translated for a UK bank or fintech review? Start with UK certified translation services, request the right format from the outset, and upload your file with the full bundle so the team can quote the fastest compliant route.

You can also point readers to:

- Certified Translation Services

- Notarised Translation

- Sworn Translation

- Certified Translation Certificate Guide

- Contact Us

“Uploaded my file in minutes and got the signed PDF back the next day. Solid service.” — Emma B.

“The team kept me updated at every step and delivered exactly what I needed.” — Maria L. (UK Certified Translations)

The bottom line

The best bank kyc document translation uk service is not the one that simply translates text fastest. It is the one that helps the reviewer confirm identity, address, and source of funds without friction.

That means:

- full-document translation, not shortcuts

- clear certification

- preserved financial detail

- secure handling

- fast delivery when deadlines are real

- the right certification level for the receiving body

If your file includes bank statements, proof of address, gift letters, company records, or cross-border funding evidence, the safest next step is to send the complete pack and ask for the exact format your reviewer can approve first time.

FAQs

What is bank KYC document translation in the UK?

Bank KYC document translation in the UK is the translation of foreign-language identity, proof of address, bank statement, and source-of-funds documents into English so a bank, lender, or fintech can review them during customer due diligence. In the UK, the translation is typically expected to be certified and independently verifiable. (GOV.UK)

Do UK banks accept certified translations for proof of address?

In many cases, yes. A proof of address translation is usually accepted when it is complete, clear, and accompanied by a proper certification statement with the translator’s details. The bank may still reject the file if the document itself is too old, incomplete, or not one of the document types it accepts. (GOV.UK)

What documents are usually included in source of funds translation?

A typical source of funds translation may include foreign bank statements, transfer receipts, gift letters, inheritance paperwork, sale agreements, dividend records, company documents, and the incoming bank record showing how the money reached the account being reviewed. The exact mix depends on the transaction story. (Solicitors Regulation Authority)

Is notarised translation required for UK bank compliance translation?

Usually not as a default. Most ordinary KYC reviews start with certified translation. Notarised translation is more likely to be requested when the receiving body specifically asks for it, or when the transaction is higher-risk, cross-border, or legally sensitive. (GOV.UK)

How fast can a bank statement or KYC translation be delivered?

Turnaround depends on the number of pages, languages, and whether the pack needs certification only or additional notarisation. UK Certified Translation states standard turnaround is 2–4 business days, with express options available. (UK Certified Translations)

What should a certified KYC translation include?

At minimum, it should include the full translated text plus a certification statement confirming accuracy, the date, the translator’s full name, and contact details. A stronger pack also keeps names consistent, preserves figures and dates, and translates stamps, notes, and visible annotations. (GOV.UK)

What is the best bank KYC document translation service in the UK?

The best bank kyc document translation uk service is usually the one most likely to produce a complete, certified, submission-ready pack for the receiving institution on the first attempt. In practice, that means accurate translation of bank statements, proof of address, source of funds, and corporate records, plus secure handling, fast turnaround, and clear certification. Rather than choosing on price alone, compare providers on compliance readiness, document-bundle handling, and whether they can explain exactly what level of certification you need. UK Certified Translation positions its service around those requirements for UK-facing document packs. (UK Certified Translations)

Can I use Google Translate or AI to translate bank KYC documents?

AI or machine translation may help you understand a document privately, but it is usually not the right solution for official KYC submission where a certified, independently verifiable translation is expected. Banks and compliance teams need a translator’s certification trail, not just English text.

Do transaction descriptions on bank statements need to be translated?

Yes, especially when the reviewer is assessing source of funds, incoming transfers, business activity, or unusual transactions. Untranslated descriptions can break the money trail even where the balances are clear.

Can I submit only the pages I think matter for KYC?

Usually not if the omitted pages contain names, dates, balances, transaction details, notes, or certification clues. KYC reviewers assess coherence and sequence, not just isolated excerpts.

Are online PDF certified translations accepted by UK banks and fintechs?

Often yes, if the institution accepts digital certified translations and the certification is complete, properly signed off, and independently verifiable. Always confirm whether the receiving body wants digital PDF, hard copy, wet ink, notarisation, or apostille before ordering.

How much does bank KYC document translation in the UK usually cost?

Cost usually depends on page count, language pair, document complexity, urgency, and whether you need certification only or extra steps such as notarisation or apostille. A bundled KYC pack is usually quoted more accurately when you send the full document set and deadline at the start.