Applying for a mortgage with documents in another language is rarely difficult because of the mortgage itself. It becomes difficult when the lender cannot read the evidence.

That is why mortgage document translation UK services need to do more than translate words. They need to turn foreign-language paperwork into a lender-ready translation pack that helps underwriters, brokers, and conveyancers verify income, assets, identity, and source of funds without unnecessary back-and-forth.

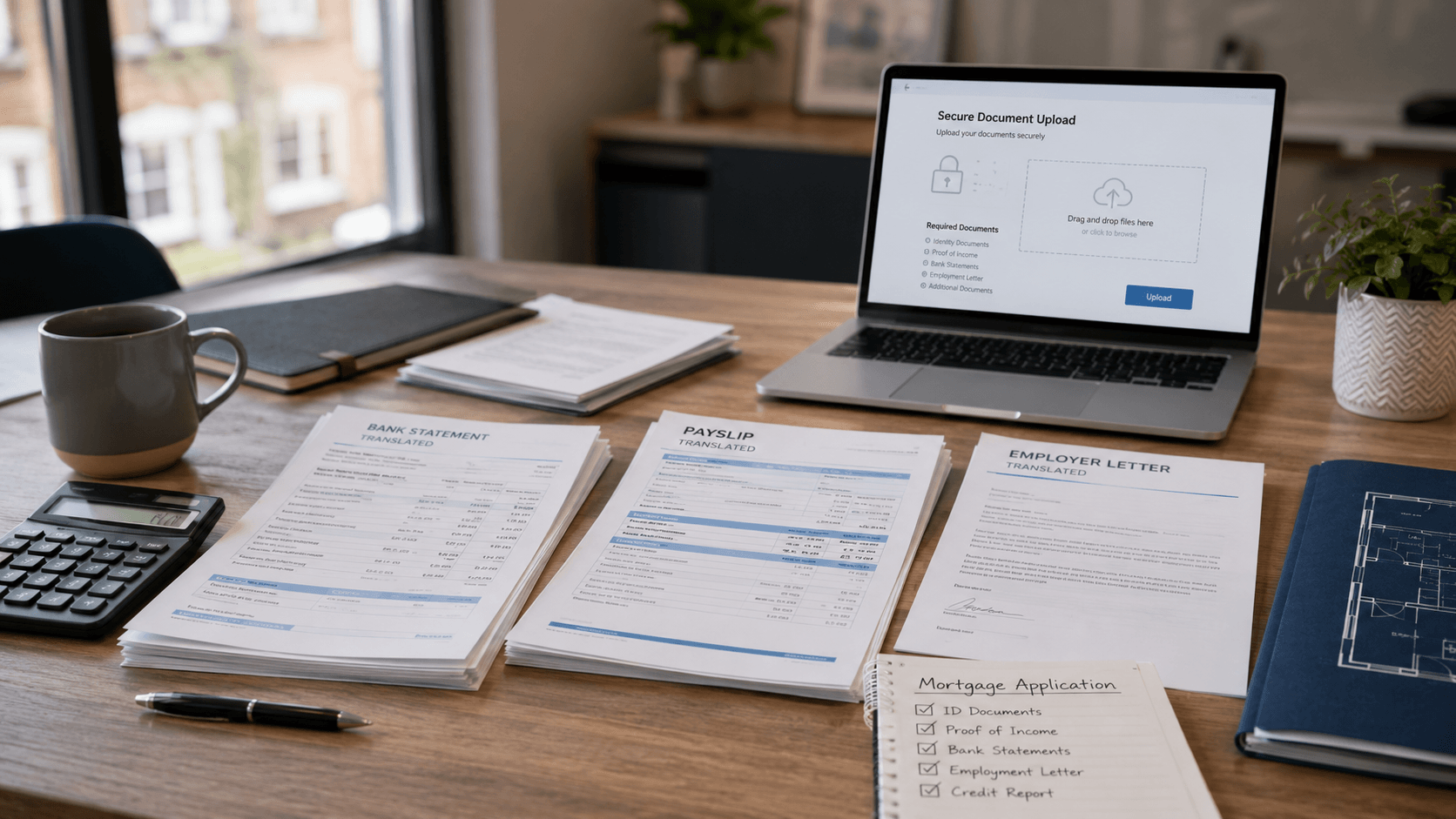

If you are preparing a mortgage application, the goal is simple: make every supporting document clear, complete, and easy to verify the first time. That includes payslips, bank statements, employer letters, tax documents, savings records, gift letters, and any proof that explains where your money comes from and how stable your income really is.

A practical way to think about mortgage paperwork is this:

Lenders do not approve translations. They approve evidence they can understand and trust.

If you need your documents reviewed before submission, upload your files for a fast quote and a format check so your translation is prepared for the way mortgage teams actually assess applications.

Do UK lenders accept translated mortgage documents?

Yes, UK lenders, brokers, underwriters, and conveyancers can review foreign-language supporting documents when the translation is complete, accurate, and suitable for official review.

In practical terms, that usually means the translation should help the reviewer verify identity, income, savings, source of funds, and document consistency without having to guess what a payroll code, bank reference, stamp, signature note, or handwritten annotation means.

For the smoothest review, it is usually better to submit a complete certified pack rather than a few isolated translated pages. A stronger pack preserves names, dates, figures, page order, account references, and supporting notes so the lender can match the translated document against the rest of the mortgage file quickly.

If your file includes income proof, bank statements, gifted deposit documents, foreign property sale records, or self-employed evidence, submitting them as one lender-ready set is often easier for the receiving party than dealing with separate pieces sent at different times.

Related reading: what is certified translation, certified translation services, how to get a certified translation, gov.uk certified translation requirements

How to choose the best company for mortgage document translation in the UK

Many people search for the best company for mortgage document translation in the UK. In mortgage cases, the best choice is usually not the cheapest word-for-word service. It is the provider that can prepare a complete lender-ready certified pack for real mortgage review.

A strong provider should be able to handle payslips, employer letters, bank statements, savings records, tax documents, gift letters, donor documents, source-of-funds evidence, and name-consistency documents as one coherent submission pack.

What to compare before choosing a provider

Check whether the provider can deliver full certified translations suitable for official use.

Check whether they translate stamps, seals, handwritten notes, and signatures rather than leaving them unexplained.

Check whether they preserve page numbering, account identifiers, transaction references, dates, and salary lines clearly.

Check whether they offer secure upload and careful handling for financial and identity documents.

Check whether they can confirm turnaround time before you order.

Check whether they include provider details for verification on the certification statement.

Check whether they can explain when certified translation is usually enough and when notarisation may only be needed if specifically requested.

Check whether they understand source-of-funds chains, gifted deposits, self-employed income packs, and cross-document name matching.

If you are comparing providers, a good test is to ask what they would flag before you submit the pack to the lender. The strongest provider is often the one that spots missing pages, inconsistent names, untranslated annotations, and weak deposit trail evidence before the lender does.

You can also support your due diligence by checking recognised professional directories when reviewing a provider.

Related reading: how to find a certified translator, certified translation services, translation services

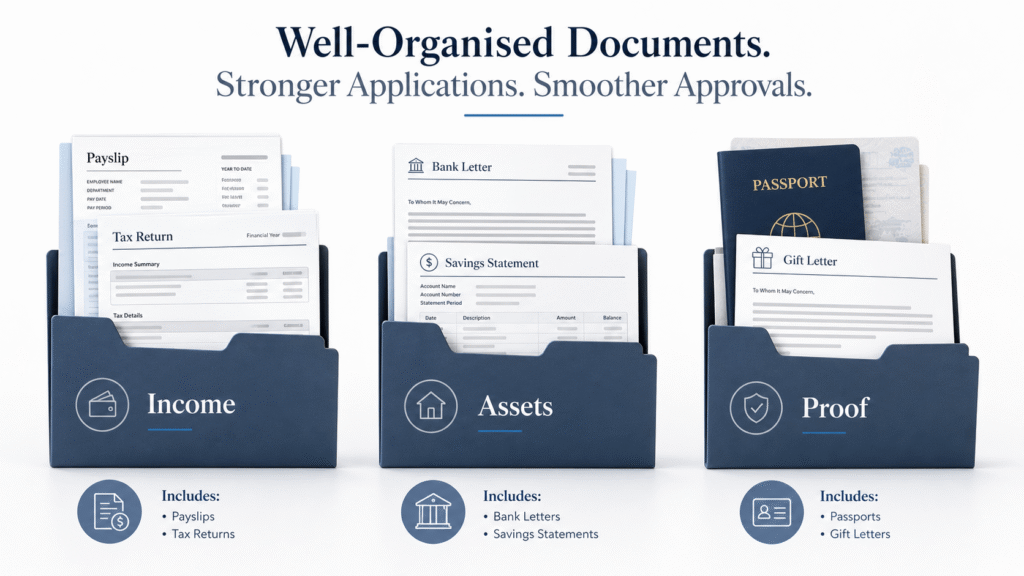

The three folders every mortgage application translation should cover

When people order translations for a mortgage, they often send documents one by one. That creates delays. A stronger approach is to build a complete pack from the start.

1. Income proof

This folder shows how you earn and whether your income is consistent.

It may include:

- recent payslips

- salary certificates

- employer references

- employment contracts

- P60s

- tax returns

- SA302s

- accountant letters

- dividend vouchers

- company accounts for self-employed applicants

This is where payslip letters translation matters most. A lender wants to see more than pay amount alone. They may need job title, employer name, payment frequency, deductions, bonuses, overtime, and dates that line up with the application.

2. Asset and source-of-funds proof

This folder explains what money you have and where it came from.

It may include:

- bank statements

- savings statements

- fixed deposit letters

- bank confirmation letters

- sale agreements

- inheritance records

- gift letters

- proof of property sale abroad

- investment liquidation records

This is where bank letters translation becomes especially important. A simple balance letter, savings confirmation, or transfer explanation can carry as much weight as a statement if it answers the exact question the lender is asking.

3. Identity and consistency proof

This folder helps the lender connect the person, the income, and the funds across every document.

It may include:

- passport

- national ID

- residence permit

- proof of address

- marriage certificate

- divorce certificate

- deed poll or name-change records

This category matters when names are spelled differently across countries, alphabets, or family records. A strong translation prevents avoidable queries like “Is this the same person?” or “Why does the surname differ on the salary slip and passport?”

What lenders usually need to understand quickly

When a lender reviews foreign-language paperwork, they are usually trying to answer a short list of practical questions:

- Who is the applicant?

- Where does the income come from?

- Is the income regular and provable?

- Where did the deposit come from?

- Do the amounts and dates match across the file?

- Is there any unexplained movement of money?

That is why mortgage document translation is not the same as ordinary document translation. The wording must be accurate, but the structure must also help the reviewer find the evidence fast.

A good mortgage translation pack makes it easy to scan:

- names

- account numbers and reference numbers

- employer details

- dates

- transaction descriptions

- balances

- incoming salary lines

- supporting notes for stamps, seals, and handwritten comments

What makes a lender-ready translation

A lender-ready translation is a translation prepared for real mortgage review, not just general understanding.

A strong lender-ready translation should include

- a full translation, not selected extracts

- clear identification of the source document

- accurate names, dates, numbers, and reference codes

- translated notes for stamps, seals, signatures, and handwritten annotations

- consistent formatting so statements and letters remain easy to compare

- a certification statement suitable for official use

- translator or provider details for verification

- delivery in the format requested, whether PDF, hard copy, or both

What it should not do

- guess unclear handwriting

- summarise only “important” transactions

- change names to sound more English

- convert currencies without clear instruction

- rewrite financial language loosely

- hide page breaks, footers, or missing pages

For mortgage files, precision beats style every time.

What the certification wording should usually cover

For UK official use, the certification statement should normally confirm that the translation is a true and accurate translation of the original document. It should also include the date of the translation and the translator’s or provider’s full name and contact details.

For mortgage files, this matters because the receiving party may want to verify not only what was translated, but also who produced the translation and how they can be contacted if a question arises.

If a lender, solicitor, conveyancer, or overseas authority asks for a higher level of formality, confirm that wording before ordering. Certified, notarised, and sworn formats are not interchangeable, and using the wrong format can create avoidable delay.

Related reading: what is certified translation, certified translation services, notarised translation services, how to get a certified translation

Payslip letters translation: where small mistakes create big delays

Payslip letters translation is one of the most common problem areas in mortgage applications because salary evidence is often checked against bank statements, tax paperwork, and employer references.

A translation should help the lender see:

- employer name

- employee name

- pay date

- pay period

- gross pay

- net pay

- tax and social deductions

- bonus or commission lines

- overtime or allowances

- year-to-date totals where shown

If the original payslip uses abbreviations, payroll codes, or country-specific deduction labels, those should be translated clearly enough for a UK reviewer to follow without losing the original meaning.

When an employer letter should also be translated

If your lender or broker has asked for additional income confirmation, translate the employer letter too. This can be especially useful when:

- your payslips do not show job title clearly

- part of your income is variable

- you have recently changed role or contract type

- your salary is paid partly in another currency

- you need to explain probation, contract renewal, or overseas employment

In many mortgage applications, the strongest evidence is not one document. It is the match between three documents: payslip, bank statement, and employer letter.

Bank letters translation and bank statement translation: what reviewers look for

Bank letters translation is often treated as a small extra, but in practice it can solve the exact question that stalls a case.

A bank letter may confirm:

- account ownership

- average balance

- savings history

- term deposit details

- release of funds

- loan closure

- mortgage balance

- source of transferred funds

Bank statement translation, meanwhile, helps prove income receipt, savings build-up, and the movement of deposit money over time.

For statements, make sure the translation preserves

- account holder name

- account number or masked identifier

- statement period

- opening and closing balances

- transaction dates

- salary credits

- transfer references

- bank branding and page numbering

- all pages, including cover or summary pages where relevant

A common mistake is submitting screenshots from mobile banking. For mortgage review, clean PDFs or properly scanned statements are far safer than cropped images.

Proof of deposit: the part many applicants underestimate

Deposit evidence is where mortgage cases can slow down quickly, especially when funds come from abroad, from family support, or from a recent sale.

Your translated proof may need to show:

- savings accumulation

- the path of the money

- the origin of the funds

- donor identity for a gifted deposit

- the relationship between donor and applicant if requested

- sale or inheritance evidence when relevant

Documents that may need translation for deposit proof

- savings account statements

- gift letters

- donor bank statements

- inheritance certificates

- probate-related documents

- property sale contracts

- completion statements

- investment redemption confirmations

If any one part of that chain stays unreadable, the whole explanation can become unclear. That is why mortgage document translation should be ordered as one evidence pack, not as isolated pages.

Self-employed mortgage applications need a different translation strategy

Self-employed applicants often assume the lender only needs translated accounts. In practice, the file may be stronger when it shows how the business story connects.

That can include:

- tax returns

- SA302 equivalents from another country

- accountant letters

- profit and loss statements

- company accounts

- dividend records

- business bank statements

- registration documents for the company

For this kind of file, consistency matters more than volume. If a tax return says one thing, the accounts say another, and the bank activity is unclear, the lender will almost always come back with questions.

A better approach is to translate the documents that explain the same income from three angles:

- what was earned

- what was declared

- what was actually received

Certified, notarised, or something else?

For most UK mortgage applications, the starting point is certified translation, not automatic notarisation.

That means the translation should be complete, accurate, and accompanied by a proper certification statement with the relevant provider details.

You may need notarisation only if a lender, solicitor, overseas bank, or another authority specifically asks for it. Ordering a more expensive format too early is not always helpful.

As a rule of thumb

- Certified translation is usually the right first route for UK mortgage support documents.

- Notarised translation is for cases where an additional layer of formal authentication is specifically requested.

- Sworn translation is more relevant in jurisdictions that require court-authorised translators.

If you are unsure, do not guess. Send the requirement wording with your documents and get the right format confirmed before the work starts.

Questions to ask before you order mortgage document translation

Before you place an order, ask your broker, lender, conveyancer, or solicitor these questions:

Do you need the full document translated or only specific documents in the pack?

Do you require certified translation, or have you specifically requested notarisation?

Do you want a certified PDF, a hard copy, or both?

Do gifted deposit documents, donor bank statements, or proof-of-relationship documents also need translation?

Do you need supporting identity records if names are spelled differently across documents?

Should the translation preserve original currency figures exactly without conversion?

Do you need the translator’s details visible on every file or only on the certification statement?

Getting these points confirmed first can save time, prevent duplicate orders, and reduce the risk of the lender coming back for extra paperwork after submission.

Related reading: how to get a certified translation, gov.uk certified translation requirements, contact UK Certified Translation

How to check a mortgage translation provider before you commit

If you are choosing between providers, ask whether they:

translate full documents rather than selected extracts only

preserve formatting and page numbering for statements and letters

include notes for stamps, seals, and handwritten annotations

offer secure upload for financial and identity documents

can prepare a full lender-ready pack for income, assets, and proof-of-funds documents

can explain turnaround clearly before the work starts

can help you avoid ordering the wrong certification level

This kind of provider-checking content gives decision-stage users a clearer answer than a generic list of agencies and increases the chance that your page is surfaced for comparison-style searches.

Related reading: how to find a certified translator, translation services

The best workflow for mortgage document translation

Speed matters in property transactions, but rushed translation without structure creates avoidable mistakes. A better workflow looks like this.

Step 1: Secure upload

Use a secure upload process and send complete files, not partial screenshots dropped across messages. Include all pages, even when some look repetitive.

Step 2: Fast quote

Ask for a fast quote based on the full pack, not one document at a time. This helps you understand timing, format, and whether any extra certification level may be needed.

Step 3: Context check

Tell the provider exactly where the translation will be used:

- mortgage lender

- broker

- underwriter

- conveyancer

- gifted deposit review

- self-employed affordability assessment

That context changes what needs special care.

Step 4: Translation and financial QA

Mortgage translations should be checked with extra attention on:

- names

- dates

- balances

- salary lines

- account references

- deposit trail documents

Step 5: Delivery in submission-ready format

Receive the file in a lender-friendly format, usually a clean certified PDF unless hard copy is specifically requested.

If your timeline is tight, start your project now and ask for the file to be prioritised as a mortgage application pack.

Need your mortgage documents checked before you submit them? Upload your files now for a fast quote and a lender-ready format check.

If your payslips, bank letters, and deposit proof come from different sources, send the full pack together and get one clear translation workflow instead of multiple delays.

Why clients look for this format:

GDPR-compliant handling

UK-accredited linguists

accepted by UK bodies

secure digital delivery

dedicated project coordinator

fast turnaround options

Related reading: how to get a certified translation, certified translation cost, contact UK Certified Translation

Seven mistakes that commonly slow mortgage applications

1. Translating only selected sections

Lenders often want the full document, not a summary of “important” pages.

2. Using self-translation or a family member

For financial evidence, independent and professionally prepared translation is the safer route.

3. Sending screenshots instead of proper files

A cropped mobile image creates doubt instantly.

4. Ignoring name inconsistencies

Different spellings, surname order, or transliteration can trigger verification questions.

5. Leaving out back pages, footers, or summary sheets

These often carry statement dates, bank branding, or reference details.

6. Ordering the wrong certification level

Certified and notarised are not interchangeable.

7. Waiting until the lender asks again

By the time the follow-up request arrives, the property timeline may already be under pressure.

Real-world mortgage translation scenarios

Scenario 1: Overseas salaried employee buying in the UK

The applicant is paid in euros, has three months of foreign payslips, and is moving funds into a UK account.

Best translation pack:

- payslips

- employer reference letter

- bank statements showing salary receipt

- ID document if names appear differently across records

Scenario 2: Self-employed director with mixed income

The applicant takes salary plus dividends from a company abroad.

Best translation pack:

- personal tax returns

- company accounts

- dividend records

- bank statements

- accountant letter if available

Scenario 3: Gifted deposit from parents abroad

The deposit is legitimate, but the lender wants a clear paper trail.

Best translation pack:

- gift letter

- donor bank statements

- transfer confirmation

- proof of relationship if requested

- source-of-funds documents where relevant

Each of these scenarios is easier when the translation is planned as one coherent evidence set instead of a patchwork of last-minute files.

A simple mortgage translation checklist before you submit

Before sending anything to your broker or lender, check that your pack answers these questions clearly:

- Can someone who does not speak the source language understand every document?

- Are names consistent across all translated files?

- Do salary amounts match bank statement entries?

- Is the deposit trail easy to follow?

- Are all pages included?

- Does the translation include a proper certification statement?

- Is the file ready in the exact format the receiving party expects?

If not, fix it before submission.

Why this matters more in mortgage applications than in many other submissions

Mortgage applications move through multiple reviewers. A broker may look first. Then an underwriter. Then compliance. Then a conveyancer may need supporting paperwork as the matter progresses.

Every extra question costs time.

That is why strong mortgage document translation is not just about language accuracy. It is about reducing friction between each reviewer and the evidence they need to approve.

When your documents are clear, complete, and lender-ready, the process becomes easier for everyone involved.

Ready to move without translation delays?

If your mortgage application includes foreign-language payslips, bank letters, statements, tax records, or proof of deposit, get the pack prepared before the lender has to chase you for missing explanations.

Upload your files through a secure upload process, request a fast quote, and ask for a lender-ready translation pack that covers income, assets, and proof in one go.

A mortgage deadline is the wrong moment to discover your evidence is readable to you, but not to the lender.

Start your project today with a secure upload and get a certified mortgage translation pack built around income, assets, and proof.

You can also ask for a format check before submission if your file includes payslips, bank letters, source-of-funds evidence, donor documents, or overseas self-employed income records.

Trust signals to place beside this CTA:

GDPR-compliant handling

secure digital delivery

UK-accredited linguists

accepted by UK bodies

dedicated project coordinator

fast turnaround options

Suggested testimonial callouts:

“Uploaded my file in minutes and got the signed PDF back the next day.”

“The team kept me updated at every step and delivered exactly what I needed.”

“Pricing was given upfront.”

Related reading: certified translation cost, contact UK Certified Translation, translation services

FAQ

Do UK lenders accept mortgage document translation UK services for payslips and bank statements?

Yes, when the translation is professionally prepared, complete, and suitable for official review. The key is that the lender can verify the information clearly and match it to the rest of the file.

What documents usually need mortgage document translation in the UK?

The most common documents are payslips, employer letters, bank statements, bank letters, tax returns, accountant letters, proof of deposit, gift letters, and identity documents where names or details need to be matched across the application.

Is payslip letters translation different from normal payslip translation?

Yes. Payslip letters translation often needs to work alongside employer letters and bank records, so the translation has to preserve payroll details, deductions, dates, and job information with extra care.

Do I need bank letters translation as well as bank statement translation?

Often, yes. A bank statement shows movement of money, while a bank letter can confirm account ownership, savings status, fixed deposits, or transfer details that make the lender’s review easier.

How quickly can I get a lender-ready translation pack?

Turnaround depends on file length, language pair, and whether you need standard certified PDF delivery or extra formalities. The fastest route is to submit the full pack together and request a fast quote upfront.

Is secure upload important for mortgage translation files?

Absolutely. Mortgage files usually contain personal and financial data, so secure upload is the safest starting point for statements, ID documents, salary records, and proof-of-funds paperwork.

What is the best company for mortgage document translation in the UK?

The best company is usually the one that can deliver a complete lender-ready certified pack for your mortgage file, not just a basic document translation. Look for experience with payslips, bank statements, source-of-funds evidence, gifted deposits, self-employed income documents, secure upload, clear turnaround, and proper certification wording.

Can I use AI or machine translation for mortgage documents?

For mortgage applications, relying on AI-only or machine-only output is risky because lenders and solicitors need complete, accurate, verifiable evidence. Mortgage packs often contain payroll abbreviations, handwritten notes, stamps, bank references, and name-consistency issues that need human review and proper certification.

Can a family member translate my mortgage documents?

That is not the strongest option for mortgage evidence. For lender and broker review, independent and professionally prepared translation is the safer route, especially where financial evidence, source of funds, identity matching, or compliance review is involved.

Do gifted deposit documents also need translation?

Often, yes. If the gifted deposit comes from abroad or the donor documents are not in English, the lender may need the gift letter, donor bank statements, transfer evidence, and sometimes proof of relationship or source-of-funds documents translated as part of one clear deposit trail.

Will my broker, lender, and solicitor all need the same translated pack?

Sometimes yes, but not always in exactly the same way. A broker may want the documents for packaging, a lender may want them for underwriting and compliance, and a solicitor or conveyancer may need supporting paperwork for source-of-funds checks. It is usually more efficient to prepare one consistent certified pack that can be used across the transaction.

How much does mortgage document translation cost in the UK?

Cost usually depends on the number of pages or words, the document type, the language pair, the certification level, the urgency, and whether you order one document or a full mortgage pack together. If your file includes statements, payslips, donor evidence, tax papers, and identity documents, asking for one quote for the full set is often the clearest way to budget.

What should a certified mortgage translation include?

A strong certified mortgage translation should include the full translated document, a certification statement suitable for official use, the date, the provider’s identifying details, and clear preservation of names, dates, figures, page order, and supporting notes for stamps, seals, and handwritten items.