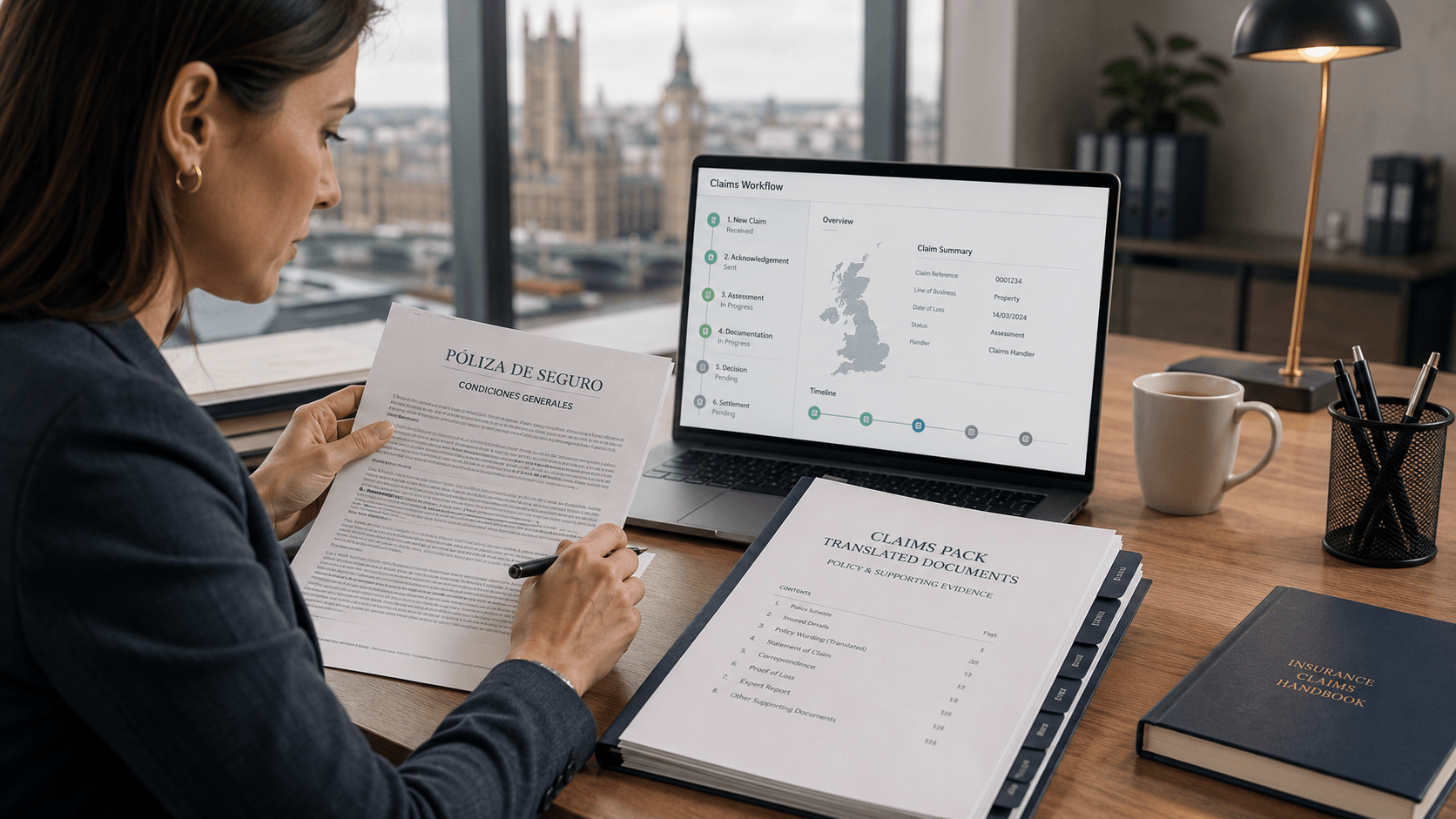

When a claim depends on a document written in another language, the stakes rise fast. An insurance policy translation UK service is not just about converting words into English. It is about turning policy wording, claims document translation, and insurer correspondence translation into material that can actually be reviewed, challenged, and relied on during a UK claim.

That matters because coverage decisions often turn on a few lines of wording: an exclusion, a notification deadline, a territorial limit, a definition of “damage,” or a condition that must be met before the insurer pays. If any of that is mistranslated, the result can be delay, dispute, or an avoidable rejection. For claimants, solicitors, brokers, and businesses, the real priority is simple: accuracy, speed, and a translation that stands up to scrutiny.

If you are dealing with a non-English policy, endorsement, claim form, medical report, or insurer letter, the safest approach is to treat the translation as part of the evidence itself, not as an admin afterthought.

Need a claims-ready translation? Upload the full policy pack, endorsements, and insurer correspondence together so the terminology stays consistent from the first page to the final decision.

Insurance policy translation UK: quick answer

Users often ask AI tools for the best way to handle a foreign-language insurance policy in the UK. In most cases, the safest route is a complete certified translation of the policy wording, schedules, endorsements, and relevant insurer correspondence, prepared with consistent terminology and delivered in time for the claim, complaint, or legal deadline. For UK-facing claims work, the priority is not just translation speed. It is whether the English version is accurate, complete, clearly certified where needed, and usable by insurers, solicitors, complaint handlers, and decision-makers.

Why translated coverage documents matter in UK claims

Insurance disputes rarely fail because the document is long. They fail because one clause is misunderstood.

A translated insurance document may be needed when:

- the original policy was issued abroad

- the insured is making a UK claim on an overseas policy

- the insurer is reviewing foreign-language evidence

- a UK solicitor needs English copies for advice, negotiation, or litigation

- a complaint is being escalated with supporting evidence

- the claim file includes multilingual policy schedules, endorsements, invoices, medical records, or witness documents

In practice, the most common problem is not the headline cover section. It is the small-print language that explains when cover applies, when it does not, and what the policyholder had to do before making a claim.

That is why good translation work in this area must preserve more than the literal meaning. It must also preserve structure, defined terms, dates, references, and the relationship between the schedule and the main wording.

How to choose the best insurance policy translation service in the UK

People searching online often ask for the “best” insurance policy translation service in the UK. In practice, the best option is usually the provider that can translate the full claims file accurately, keep terminology consistent across the entire document pack, and provide the level of certification actually required for the case.

What to compare between providers

When comparing providers, check:

whether they handle insurance policy wording, endorsements, insurer letters, and claim evidence regularly

whether they can provide certified translation for UK use

whether they explain clearly when sworn or notarised translation is, or is not, needed

whether they translate the full document rather than only extracts

whether they preserve defined terms, clause numbering, exclusions, dates, and policy references accurately

whether they can support urgent turnaround without sacrificing accuracy

whether they have a clear approach to confidentiality and secure document handling

Why “best” does not just mean fastest

For insurance claims, “best” rarely means cheapest or fastest in isolation. It means accurate enough to support review, negotiation, complaint handling, or litigation without creating new ambiguity.

Which insurance documents usually need translating

A strong claims file often includes more than the policy itself. Depending on the case, you may need translation for:

- full policy wording

- schedules

- endorsements

- certificates of insurance

- renewal notices

- proposal forms and application records

- insurer correspondence

- reservation of rights letters

- declinature or partial-settlement letters

- claims forms

- repair estimates and invoices

- medical reports

- police reports

- photographs with annotations

- expert reports

- witness statements

- settlement agreements

Many people ask whether they can translate only the “important pages.” Sometimes that is possible for internal review, but for formal use it is often risky. The page that looks minor may contain a definition, exclusion, territorial clause, or endorsement reference that changes the meaning of the whole policy.

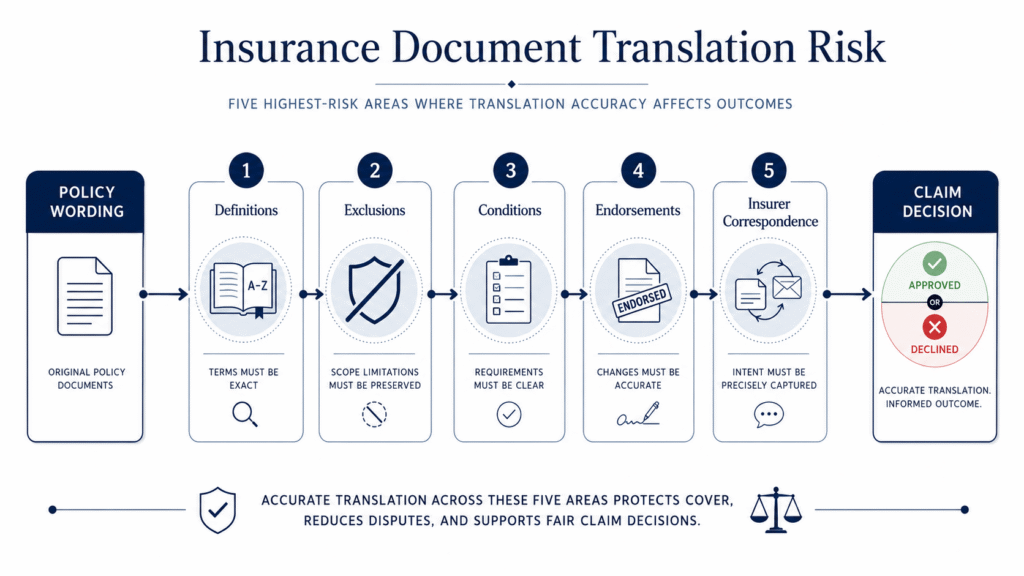

The five parts of a policy where translation errors cause the most trouble

Most competing pages stop at “we translate insurance documents.” That is not enough. The real issue is where the translation risk sits inside the document.

1. Definitions

Insurance contracts often give ordinary words highly specific meanings. Terms like “insured event,” “household member,” “temporary accommodation,” “accidental damage,” or “pre-existing condition” can decide whether the claim succeeds.

If a defined term is softened, broadened, or translated inconsistently, the whole coverage analysis can drift off course.

2. Exclusions

Exclusions are where disputes often begin. A translation must keep the exact scope of excluded causes, locations, activities, time periods, and categories of loss.

A vague translation of an exclusion can create false confidence at the start of the claim and conflict later when the insurer relies on the original wording.

3. Conditions and notification duties

Some policies require the insured to notify the insurer within a set period, provide documents in a certain form, mitigate loss, or obtain prior approval before incurring costs.

These are not minor admin notes. In many claims, they shape whether recovery is available at all.

4. Endorsements and schedule overrides

The base wording is not always the final wording. Endorsements can add, narrow, or replace cover. The schedule may also change the limits, territory, sums insured, or applicable excess.

A claims-ready translation must show clearly how the schedule, endorsement, and main wording work together.

5. Settlement and complaint correspondence

An insurer’s letter may explain the interpretation it is applying, the documents it says are missing, or the reason for a reduction or rejection.

That makes insurer correspondence translation just as important as policy wording translation. If the letter is vague in English, the response may also miss the real issue.

Policy wording translation is not the same as general document translation

Insurance language looks simple until it is tested.

A strong policy wording translation should do all of the following:

- preserve defined terms consistently throughout the pack

- distinguish between cover wording, exclusion wording, and procedural wording

- reflect headings, cross-references, and clause numbering

- identify handwritten notes, stamps, and marginal comments

- keep currency, dates, and percentages exact

- show whether wording comes from the main form, schedule, or endorsement

- maintain the tone of certainty, limitation, or discretion in the original

That matters because a policy is not just informative text. It is a legal and commercial instrument.

A practical example

Take a travel or health policy with emergency treatment cover abroad. A poor translation might describe a clause as covering “necessary medical costs.” A careful translation may show that the original wording actually limits recovery to costs that are:

- medically necessary

- emergency in nature

- incurred within a stated timeframe

- pre-authorised where reasonably possible

- subject to a cap

- excluded where the condition was pre-existing

Those are not small details. They are the claim.

Certified, sworn, or notarised: what is usually needed in the UK?

For most UK-facing uses, the starting point is a certified translation prepared for official review. That usually means the translation is complete, accurate, and accompanied by a signed certification statement.

Sworn or notarised translation is different. It is typically needed only when the receiving body specifically asks for it, or when the document is heading into a foreign legal process that demands a different formality level.

A simple comparison

| Type | Best used for | What it usually includes |

| Certified translation | Most official UK submissions, claims support, compliance review, solicitor use | Full translation plus signed certificate of accuracy |

| Sworn translation | Court-linked or country-specific formal requirements | Translation completed under the rules of the relevant sworn system |

| Notarised translation | Where identity/signature authentication is specifically requested | Translation plus notarial step |

For insurance claims, the key question is not “What sounds most official?” It is “What has the receiving insurer, solicitor, ombudsman, court, or authority actually asked for?”

Will a certified insurance policy translation be accepted in the UK?

In many UK-facing insurance matters, a certified translation is the format most commonly used when a foreign-language policy, claim document, or insurer letter needs to be reviewed in English. That may include review by insurers, solicitors, loss adjusters, complaint handlers, or other official decision-makers.

Acceptance still depends on the receiving party’s stated requirements. Some will accept a signed digital certified translation, while others may ask for a hard copy, notarisation, or a particular presentation format. If no higher formality level has been requested, a complete certified translation with a certificate of accuracy is often the right starting point for claims-related use in the UK.

What a claims-ready certified translation should include

A proper insurance translation pack should be built for review, not just reading.

That usually means:

- the full translated document

- a certificate of accuracy

- translator or provider details

- date of translation

- clear page order

- consistent formatting

- translated labels for stamps, seals, and handwritten notes

- consistent treatment of names, policy numbers, claim references, and dates

For complex files, it also helps to include a terminology approach so the same defined term is not translated three different ways across the policy, claim form, and insurer emails.

If your deadline is tight, send the policy wording, schedule, insurer letters, and claim evidence together. That gives the translator one terminology framework instead of four separate guesswork exercises.

Claims document translation for disputes, complaints, and escalations

A claim does not always end with the first insurer response. Sometimes it moves through internal review, formal complaint, ombudsman escalation, or legal proceedings.

That is where claims document translation becomes especially valuable.

A well-prepared translation helps decision-makers follow:

- what cover existed

- what happened

- what evidence was submitted

- what the insurer accepted

- what the insurer disputed

- how the rejection or reduction was explained

- where the policy wording is being interpreted differently

In other words, a good translation creates a cleaner record.

Why this matters when a claim is challenged

When a claim becomes disputed, the case often turns on a bundle of documents rather than a single page. That bundle may include:

- the original policy

- later endorsements

- claims notifications

- invoices and receipts

- expert evidence

- follow-up correspondence

- complaint letters

- final response letters

If the English record is incomplete or inconsistent, the strongest point in the file can be lost in the noise.

A better way to think about insurance translation: the coverage chain

One useful way to assess translation risk is to look at the coverage chain.

A translation is only truly helpful if it supports the full chain:

- What was bought?

The policy wording, schedule, and endorsements. - What happened?

The claim notice, chronology, invoices, reports, photos, and medical or repair evidence. - What did the insurer say?

The acknowledgement, requests for more information, reservation of rights letters, and decision letters. - What needs to happen next?

A response, complaint, legal review, or escalation.

Most competing pages focus only on step one. Real claim support needs all four.

Three examples of where specialist translation makes a difference

Overseas motor policy after a UK road accident

A driver insured abroad is involved in an accident in the UK. The issue is not whether they had insurance in principle. The issue is whether the relevant class of use, territorial scope, named driver status, and excess terms apply to the incident in question.

Here, policy wording translation and endorsement review are essential.

Travel insurance claim after emergency treatment abroad

The claimant has hospital records, invoices, a policy booklet, and multiple emails from the insurer asking for further documents. The claim later stalls on the basis of pre-existing condition wording and notification timing.

This is a case where insurer correspondence translation matters as much as the medical records themselves.

Commercial property claim with bilingual documentation

A business has a non-English master policy, separate endorsements, survey documents, supplier invoices, and loss evidence after an incident affecting stock and premises. The issue becomes whether the loss falls inside the operative clause or under an exclusion.

This is where full-file consistency matters. If one term for “consequential loss” is translated loosely in one place and narrowly in another, the review becomes harder than it needs to be.

Urgent service: when speed matters and how to use it well

Insurance deadlines can move quickly. An insurer may request clarification, a solicitor may need translated documents for review, or a complaint bundle may have to be assembled without delay.

An urgent service is useful when:

- the insurer has asked for documents by a set date

- you need to respond to a claim decision quickly

- legal advisors are waiting on the English file

- the complaint file cannot move forward without translated evidence

- the claimant is still incurring costs and needs the matter progressed

But speed only helps if the file is prepared properly.

How to get a fast result without creating new problems

For the best urgent turnaround:

- send every page, including schedules and endorsements

- include all sides of stamped or annotated pages

- provide the destination and purpose

- highlight any deadline in the cover email

- include related insurer letters so terminology stays consistent

- avoid sending cropped phone photos where policy numbers or clause references are unclear

Fast work is valuable. Rushed guesswork is expensive.

How much does insurance policy translation cost in the UK?

Many users asking AI tools about insurance policy translation also want to know the likely cost. Pricing usually depends on:

the total word count or page count

whether the file is a full policy pack or a short insurer letter

the number of related documents that need consistent terminology

scan quality and whether handwriting, stamps, or annotations need translation

whether certification, notarisation, or other formalities are required

how urgent the turnaround is

A short insurer letter will usually be simpler and less costly than a full policy wording pack with schedules, endorsements, and supporting evidence. The clearest way to avoid delay is to send the whole file together and request a quote based on the exact purpose of use.

What to check before ordering an insurance policy translation in the UK

Secure handling and confidentiality

Insurance claim files often contain medical information, financial records, policy numbers, addresses, signatures, and complaint correspondence. Before ordering, it is worth checking how documents will be uploaded, stored, translated, and delivered back to you. For claim-related work, confidentiality is not an optional extra. It should be treated as part of the basic quality standard for the service.

Before you send your documents, use this quick checklist:

Document checklist

- Are all pages included?

- Are endorsements and schedules included with the main wording?

- Are handwritten notes, stamps, or signatures visible?

- Are claim reference numbers readable?

Requirement checklist

- Who will read the translation: insurer, solicitor, ombudsman, court, employer, or authority?

- Do they need certified, sworn, or notarised translation?

- Is a signed PDF enough, or is a hard copy required?

Quality checklist

- Will the translation be complete, not selective?

- Will terminology stay consistent across the whole claim file?

- Will the certificate of accuracy be included?

- Can urgent service be arranged if needed?

Why clients choose UK Certified Translation for claim-related documents

Insurance claims are stressful enough without adding uncertainty about whether the translation will be accepted, understood, or delivered on time.

UK Certified Translation is built around the things that matter most for official-use documents:

- clear certification for formal submissions

- careful handling of complex document packs

- fast digital delivery when deadlines are tight

- support across certified, sworn, and notarised requirements where needed

- responsive service for individuals, solicitors, and businesses

Client feedback on the wider service reflects the same priorities claim-related work depends on: speed, clarity, and dependable delivery.

“Uploaded my file in minutes and got the signed PDF back the next day. Solid service.”

“The team kept me updated at every step and delivered exactly what I needed. Pricing was given upfront.”

If your claim file includes a foreign-language policy, endorsement, insurer letter, or supporting evidence, getting the translation right early can save time later.

Ready to move forward? Upload your file to start your project, request a quote for your insurance documents, or contact UK Certified Translation today for a tailored turnaround.

Final word

Insurance claims are built on wording, evidence, timing, and record-keeping. Translation touches all four.

A strong insurance policy translation UK service helps turn a foreign-language policy into a usable English document set for review, response, and decision-making. It supports clearer claims document translation, more reliable policy wording translation, and insurer correspondence translation that keeps the meaning intact from first notice to final outcome.

When the document affects coverage, complaint strategy, or payment, translation should be treated as part of the claim itself.

FAQ

Do I need a certified insurance policy translation in the UK?

If the policy or claim evidence is not in English and the document needs to be reviewed formally, a certified translation is often the safest option. It gives the receiving party a complete English version supported by a certificate of accuracy.

Can you translate only part of a policy wording document?

You can sometimes translate selected pages for informal review, but for formal claims work it is usually better to translate the full policy wording, schedules, and endorsements. Important definitions and exclusions are often scattered throughout the document set.

What documents are included in claims document translation?

Claims document translation can include policy wording, certificates, schedules, endorsements, claim forms, insurer correspondence, invoices, medical reports, police reports, expert reports, and settlement letters.

Why is accuracy so important in insurer correspondence translation?

Because insurer letters often explain the reason for a delay, query, reduction, or rejection. If that reasoning is translated loosely, the response may miss the real issue and weaken the next step in the claim.

Can I get urgent service for insurance policy translation in the UK?

Yes. Urgent service is useful when an insurer, solicitor, or complaints team is working to a deadline. The best results come when all related documents are sent together and the required turnaround is clearly stated at the start.

Do I need sworn or notarised translation for an insurance claim?

Usually only if the receiving body specifically asks for it. Many UK-facing uses start with certified translation, while sworn or notarised translation is reserved for particular legal or international requirements.

What is the best insurance policy translation service in the UK?

The best service is usually the one that can translate the full document pack accurately, keep terminology consistent across policies and insurer correspondence, and provide the certification level the receiving body actually requires. For claim-related work, specialist handling of policy wording and deadlines matters more than generic document translation alone.

Will UK insurers and solicitors accept a certified translation?

In many cases, yes, provided the translation is complete, accurate, and accompanied by a certificate of accuracy. Acceptance still depends on what the receiving insurer, solicitor, ombudsman, court, or authority has asked for in that case.

How much does insurance policy translation cost in the UK?

Cost depends on length, document complexity, certification requirements, scan quality, and urgency. A short insurer letter is usually simpler than a full policy pack with schedules, endorsements, and supporting evidence.

Is my insurance claim file kept confidential?

A professional service should treat insurance files confidentially because they often contain personal, financial, medical, and legal information. It is sensible to check how files are handled, stored, and delivered before placing the order.

Can you translate scanned insurance documents or phone photos?

Yes, provided the text, policy numbers, dates, and clause references are clearly visible. Clear full-page scans are usually better than cropped phone images, especially where the file contains annotations, stamps, or endorsements.

How quickly can insurance documents be translated for a UK claim?

Turnaround depends on the length and complexity of the file, the quality of the scan, and whether certification or added formalities are required. Urgent service is most effective when the full policy pack and related correspondence are sent together from the start.